These platforms facilitate accurate record-keeping and enhance the overall efficiency of inventory operations. Perpetual inventory is computerized, using point-of-sale and enterprise asset management systems, while periodic inventory involves a physical count at various periods of time. The latter is more cost-efficient, while the former takes more time and money to execute.

Documenting Transactions and Purchases

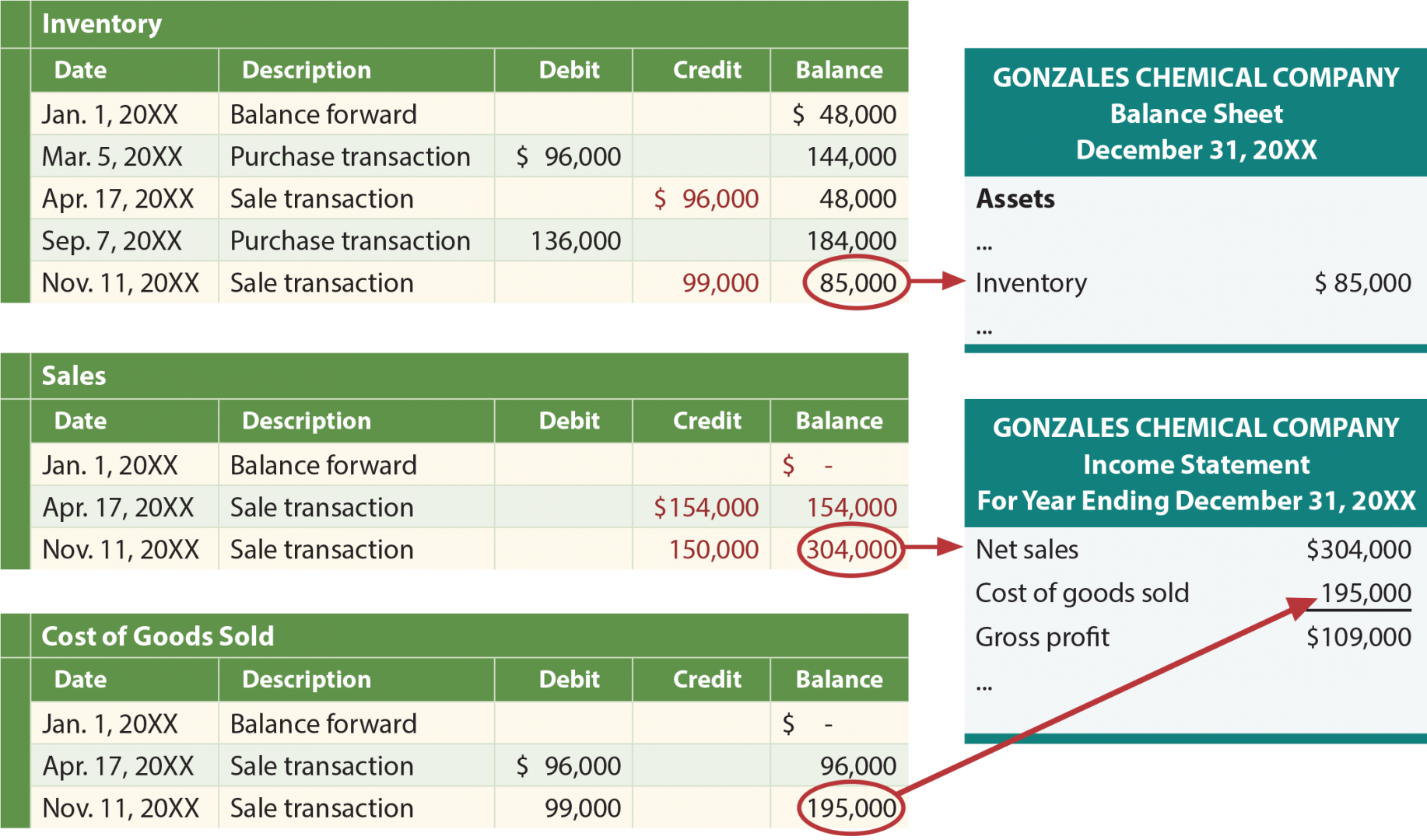

The Inventory balance is $352.50 (4 books with an average cost of $88.125 each). If your business deals with high-value items or products that sell quickly, using a perpetual inventory system allows you to maintain accurate and real-time stock levels. This helps prevent stockouts and ensures optimal customer satisfaction. Throughout this guide, you’ll learn about the key differences between a perpetual system and periodic inventory systems. We’ll also discuss the pros and cons of using a perpetual inventory system in various scenarios.

AccountingTools

For example, suppose a shop sells one of the two identical pairs of shoes in its inventory. One pair cost $5 and was purchased in January, and the second pair was purchased in February and cost $6 unit. Under the LIFO method, the value of ending inventory is based on the cost of the earliest purchases incurred by a business. This is why LIFO creates higher costs and lowers net income in times of inflation.

- $14,000 plus $7,740 plus $5,160 gets us to our total cost of goods sold of $26,900.

- Let’s say on January 1st of the new year, Lee wants to calculate the cost of goods sold in the previous year.

- This can be done manually using spreadsheets; however, modern companies often opt for specialized software solutions like QuickBooks, NetSuite, or TradeGecko.

- Therefore value of inventory using LIFO will be based on outdated prices.

Benefits/Improved Cash Flow:

So you saw here with the perpetual, that average moves after each purchase, right? We’re going to see that the average changes after each purchase in this case. LIFO perpetual inventory is an accounting method that affects how businesses track and value their inventory. Its significance lies in its impact on financial statements, tax liabilities, and overall business strategy. As companies strive to manage costs effectively, understanding LIFO can provide insights into optimizing inventory management. Inventory refers to any raw materials and finished goods that companies have on hand for production purposes or that are sold on the market to consumers.

Both are accounting methods that businesses use to track the number of products they have available. Keeping track of all incoming and outgoing inventory costs is key to accurate inventory valuation. Try FreshBooks for free to boost your efficiency and improve your inventory management today. In a perpetual inventory system, FIFO (First-In, First-Out) and LIFO (Last-In, First-Out) are methods used to track inventory and cost of goods sold (COGS). FIFO assumes that the oldest inventory items are sold first, so COGS reflects the cost of older inventory.

Conversely, LIFO assumes that the newest inventory items are sold first, so COGS reflects the cost of newer inventory. This difference impacts financial statements, especially in periods of price fluctuation. FIFO typically results in lower COGS and higher net income when prices are rising, while LIFO results in higher COGS and lower net income. Most companies use the first in, first out (FIFO) method of accounting to record their sales. The last in, first out (LIFO) method is suited to particular businesses in particular times. That is, it is used primarily by businesses that must maintain large and costly inventories, and it is useful only when inflation is rapidly pushing up their costs.

As inventory is stated at outdated prices, the relevance of accounting information is reduced because of possible variance with current market price of inventory. Properly managing inventory can make or break a business, and having insight into your stock through the perpetual inventory method is crucial to success. Regardless of the type of inventory control process you choose, decision-makers know they need the right tools in place so they can manage their inventory effectively.

For instance, grocery stores or pharmacies tend to use perpetual inventory systems. The periodic inventory system is often used by smaller businesses that have easy-to-manage inventory and may not have national real tax tracking company profile a lot of money or the opportunity to implement computerized systems into their workflow. As such, they use occasional physical counts to measure their inventory and the cost of goods sold (COGS).

If LIFO affects COGS and makes it more significant during inflationary times, we will have a reduced net income margin. Besides, inventory turnover will be much higher as it will have higher COGS and smaller inventory. Also, all the current asset-related ratios will be affected because of the change in inventory value. A company may prefer using a FIFO system when it’s trying to show its largest possible profit on its financial statements for investors, lenders and stakeholders. Inventory management formulas can tell you when to order more inventory, how much to order, the lead time needed before placing an order and how much stock you require to keep in safety. A typical journal entry would show which account the software debited and which account the software credited for each transaction.

Leave a Reply